The Two Opinions Conundrum

FEATUREDINTERNAL AUDITSOXCOMPLIANCE

Do material weaknesses drive financial statement material misstatements? – Not always the case.

The Two Opinions Conundrum

Ever wondered about the correlation between Failed Audits and Material Weaknesses? - The analysis has been done and provides a counterintuitive finding from 5 years of SEC 10-K data:

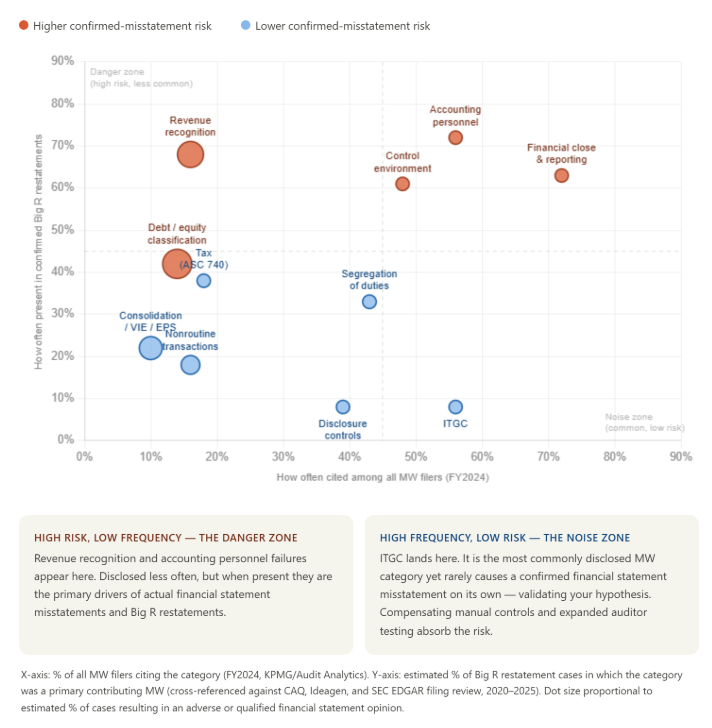

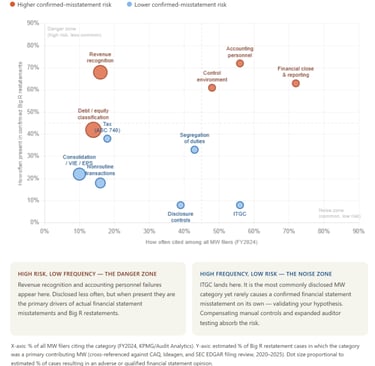

ITGC weaknesses are cited in 56% of all material weakness disclosures — yet appear as a primary driver in fewer than 10% of confirmed financial statement restatements.

Revenue recognition control failures? Cited in only 16% of disclosures — but present in ~68% of confirmed Big R restatements.

The chart below plots every major MW category by how often it's disclosed vs. how often it actually causes a confirmed misstatement. The inversion is stark.

The takeaway for audit committees and SOX teams: frequency of disclosure is a poor proxy for financial reporting risk. The categories that should command the most remediation urgency — accounting personnel gaps, revenue recognition controls, and control environment failures — are not always the ones generating the most compliance noise. ITGCs matter. But they are rarely the reason a company's financial statements are wrong.

So, what can you do? - Take a risk-based approach and align more human effort with the most likely misstatement drivers that require more judgment and leverage Agentic AI solutions for transactional lower-risk control testing like ITGCs. We now have the tools to make this shift and the reasons for doing so are compellingly supported by the data.

Analysis based on KPMG's 2024 Material Weakness Study (Audit Analytics data), the CAQ's Financial Restatement Trends report (2024), and Ideagen Audit Analytics annual restatement studies, 2020–2024. Research assisted by Claude (Anthropic).

Ian Burnett is the Founder of Risk Boundary Advisors LLC, a provider of consulting expertise in GRC, Internal Audit, SOX, and Controls Optimization. He is an experienced executive with diversified experience in risk management, auditing, finance, consulting and investment banking. Learn more about Ian on LinkedIn.

These are the opinions of the editors of Internal Audit Next and/or the writer who authored this article. Any use of this copyrighted material without permission of Internal Audit Next - including training for AI Models - is prohibited. Copyright 2026.

Related Articles

Internal Audit Next © 2026

Internal Audit Next is a site containing thought leadership articles for the GRC (Governance, Risk, and Compliance) industry. Staffed and written by volunteers looking to change this industry for the better.